2026 Winter Cattle Journal | 2026 Cattle and Beef Market Prospects

Cattle and beef prices set new records in 2025 before facing a significant setback late in the year. High beef prices were the subject of intense political and public scrutiny in the fourth quarter of 2025. Though cattle markets are in a correction late in 2025, strong supply and demand fundamentals are expected to push cattle prices to new highs in 2026.

Cattle Cycle Status

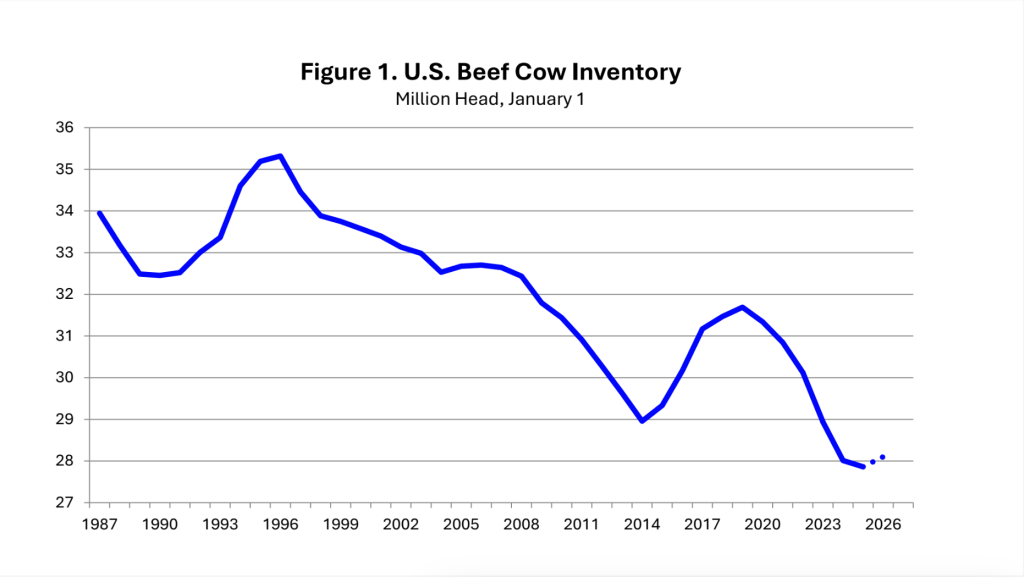

Coming into 2025, the beef cow herd totaled 27.86 million head, the lowest inventory since 1961. This follows six years of drought-enhanced liquidation since the most recent peak in 2019 that saw a herd decrease of 3.78 million head, down 11.9 percent in the last six years (Figure 1). There are indications that the beef cow herd is stabilizing at the current level and the 2025 inventory may be the cyclical low for this cattle cycle (eleven years after the previous low in 2014). The beef cow herd is stabilizing because beef herd culling has dropped to low enough to avoid further liquidation. Beef cow slaughter in 2025 is projected to be down nearly 41 percent from the recent peak in 2022, and would represent a national culling rate under 8.5 percent, down from the 2022 record culling rate of 13.2 percent. Decreased cow culling is one of the factors needed for a cyclical inventory low before the next herd expansion. The 2026 January 1 beef cow inventory may be just slightly higher year over year, making 2025 the cyclical low, eleven years after the previous low in 2014.

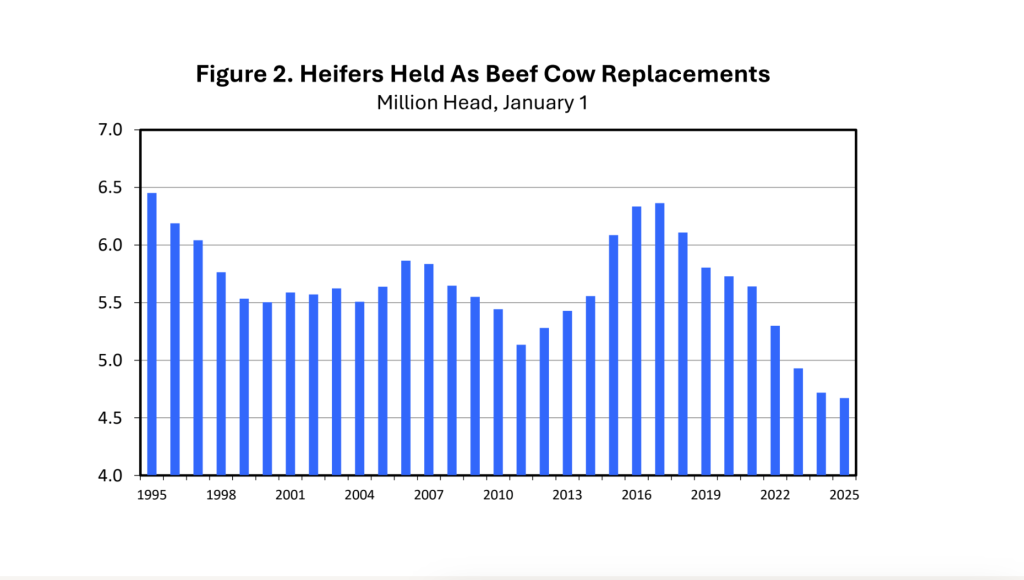

However, beef cow herd expansion requires heifer retention. The inventory of beef replacement heifers has continued to decline since 2017 (Figure 2). While the beef cow herd may be stabilizing, the lack of beef replacement heifers means that no significant herd growth is possible in 2026 and very likely in 2027 as well. In the closing weeks of 2025, there is no evidence that any significant heifer retention has started in 2025. It appears that the industry continues on a delayed and slow process of herd rebuilding that will likely take until the end of the decade.

Cattle on Feed

Seven years of declining calf crops have resulted in extremely tight feeder cattle supplies that pose additional challenges for feedlots. The 2025 U.S. calf crop is projected to be the smallest since 1941. Try as they might to maintain inventories, feedlot numbers inevitably will come down. In November, the feedlot total was 11.7 million head, down two percent year over year. The average monthly feedlot inventory for the past year is at the lowest level since November 2018 and is expected to continue decreasing in the coming months. October feedlot placements were the lowest on record and average placements for the past year have been the lowest since July 2016.

Beef Production and Consumption

Total beef production is projected to decrease roughly 4.5 percent year over year in 2025 and is forecast to decrease about that same amount in 2026 and 3.5 – 4.0 percent in 2027. Fed steer and heifer carcass weights have increased sharply in 2024 and 2025 and will continue to increase. However, decreased fed slaughter will ensure that beef production continues to fall. Nonfed beef production, from cull cows and bulls, has been falling the most dramatically since 2022. Nonfed beef production is projected to be down 8.3 percent year over year in 2025, a decrease of 25.0 percent since 2022.

Per capita beef consumption will decrease as beef production falls. Consumption is projected at 59.0 pounds (retail weight) in 2025, down from 59.7 pounds last year. Increased net beef imports partially offsets decreased domestic beef production. Per capita beef consumption is forecast to drop below 55 pounds by 2027.

Cattle and Beef Trade

Beef exports decreased as expected after peaking in 2022 with lower beef production and higher prices but the decrease was aggravated in 2025 by tariffs and trade wars. Most notably, the U.S. is essentially out of the market in China at the current time. The impact of reduced beef exports was masked by the very dynamic domestic market and record prices in 2025

Beef imports were a source of much discussion and political focus late in 2025. Beef imports increased as expected but were impacted by broad-based tariffs. Brazil, the largest source of beef imports early in 2025 was hit with sharply increased tariffs in August that were removed in late November. Most beef imports are lean processing beef that supports the ground beef market in the U.S.

Beef Prices

Reduced beef supplies, combined with persistently strong beef demand have pushed retail beef prices to ever higher levels in 2025. Record retail beef prices in 2025 received intense political scrutiny as a part of broader focus on food prices and inflation. While the federal government is trying several actions and making lots of market-rattling comments, the fact is that there is nothing political that will change beef prices quickly. In fact, beef prices are destined to go even higher as beef production continues to fall in the coming months.

Tariff changes in late 2025 is expected to boost beef imports somewhat relative to the fall period (when Brazil was facing incredibly high tariffs). This may slightly moderate imported lean trimmings values which have been high relative to domestic lean (nonfed) beef markets. However, most imported beef is used for ground beef in the food service sector and no impact is expected on retail grocery hamburger prices and certainly not on steak or other beef product prices.

Cattle Prices

After setting new records through much of 2025, cattle prices were pummeled by a barrage of political attention and speculation that sharply reduced cattle futures and cash markets. External factors dominated and overwhelmed market fundamentals late in the year. However, the fundamentals remain in place and are expected to regain control in the coming year. The forecast is for higher average feeder and fed cattle prices in 2026 resulting from continued strong supply and demand fundamentals. Volatility is likely to remain high as well adding to the challenges for the industry to manage cattle production and marketing.

Outlook by Sector

Market prices are focused on providing incentives for herd rebuilding. Cow-calf producers control supply for the entire industry and record cow-calf returns are strong market signals for heifer retention. It has been very slow thus far and strong returns are expected to continue in 2026 and likely beyond.

Above the cow-calf level, the industry consists of margin operations where the buy-sell spread is more important than absolute price level. The margins are more challenging because the input side is increasing faster than the output side most of the time. Thus, for example, stocker/backgrounding values of gain are much less attractive compared to calf values. Forage has the most value for calf production with less incentive for stocker-based forage gains.

Feedlots have fared reasonably well as cattle prices have risen, with the uptrending market and extended days on feed providing a better “buy now – sell later” margin. Decreasing feedlot cost of gain has also helped feedlots maintain better profitability. Going forward, the ever-tighter feeder cattle supply and high feeder prices will reduce feedlot inventories and returns. Increased heifer retention at some point will squeeze feeder supplies to the tightest level.

Beef packers have born most of the brunt thus far with extended and continuing losses that will continue and get worse. The late November announcement by Tyson to close the Lexington, Nebraska plant and reduce operations at the Amarillo, Texas plant reflects the ongoing operational challenges of beef packers. Beef retailers will likely see margins squeezed more going forward as the ability to pass on higher wholesale beef costs is limited.